The Logistics Behind Plunge - $200M in Sales in 4 Years.

Plunge is doing a public raise on WeFunder.

They’ve raised 40M from 400 independent investors at a $90M valuation.

They did $82M in revenue and -5M in net loss in 2024.

This post is a deep dive on their supply chain & road to profitability.

What Do They Sell?

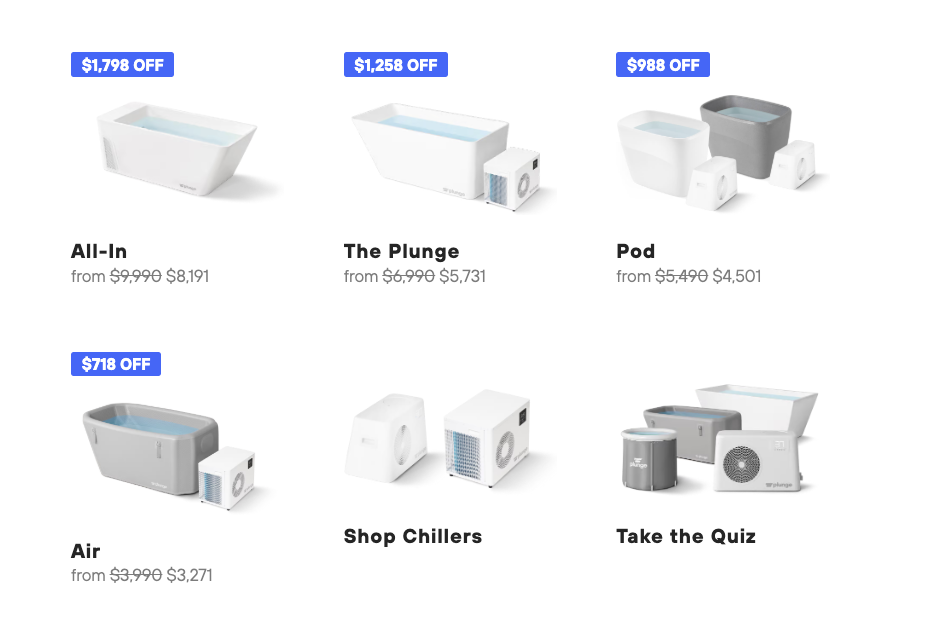

Ice Baths

Their ice bath product line is 5 models & makes up the majority of revenue. Prices range from $1k to $12,000k.

Sauna’s

Their sauna product line is on the rise. 2 models. Prices range from $10k to $20k.

Accessories

To increase AOV, they sell things ~ 50 things that go with the main stuff. Think platforms, heaters, chlorine maintenance, mini trampolines, neck pillows etc.

Replacement Parts

Lots of electronics to power Ice Baths & Sauna’s. That means lots of replacement parts. I’d estimate 300+ total.

Operational Strategy

This brand has gone BIG. $200M in just 4 years.

#1 - Many Core Focuses - Ice Bath’s, Sauna’s, Accessories, Consumer App, B2B App, B2B Sales.

#2 - Big Team In House - $10M in 2024 payroll.

#3 - High COGS - Gross Margin’s of only 37%

As a result, they were sitting at -$5M EBITDA for 2024. Will they become profitable?

I believe so. If their team can identify inefficiencies and ruthlessly attack them, they will find $5M+ in savings.

Product in Focus - The All-In Plunge

Estimated. No insider information.

Manufacturing

Country of Origin - Unknown.

Comparables - $3k via Alibaba for high-end model.

Tariffs

58.5% (28.5% category-based + 30% Trump tariff).

Ocean + Truck-> Roseville CA

37 units per 40 ft container | 1 unit per pallet.

est. $5000 ocean to ocean.

238 lbs, 77x32x29 inches for 1 unit.

Final Mile Distribution

Via LCL freight from Roseville, CA

Planning to expand international (local distribution) in 2025/2026 (source)

——————-

I calculated their Gross Margin’s with this template -> DTC Landed Cost Template